Retirement is the last thing on our minds when we initially start out to build our careers. Seriously, not many start their career Planning for Retirement early.

But no matter how cool “living in the moment” sounds, one should consider one’s retirement at the earliest point in their careers. Having a mid-life crisis without the slightest idea about your future or your retirement plans, is the last thing you need. Of course planning for retirement does not have to be on your mind constantly, that would only add to your stress. But it is an important factor to be considered every time you make an important career or life decision.

Here are a few tips to guide you while planning for your retirement early in life.

1. The “Why” question:

Why should I plan for my retirement early on?

In fact, why should I “plan” for my retirement at all?

First of all, it is important to understand that planning for your retirement does not just mean the financial aspect of it. It is as important to have personal plans as well. When you have the time and freedom to do anything with your life, it can be liberating; but also overwhelming!

Without a plan on what to do, you might either be bored out of your mind, or restless from deciding on what you want to do (out of the many things you have always wanted to do but could not because of your job or schedule). Therefore, good retirement planning must comprise of financial AND personal plans.

The age factor

Secondly, with age comes new health problems and medical issues.

Medical expenses can hit your finances pretty hard, so it is better to have a solid retirement plan that will have you well taken care of.

Plan early to beat inflation

Inflation is another reason to start retirement planning early on. It is usually underestimated, but especially in a country like India, inflation is a fact and the effects will be felt in the long term. Even if you plan to live your retirement on a strict budget, every day bills will catch up to you.

Moreover, in India, the social security plans are meagre to fully aid our financial security. One cannot depend on it. Hence, the need to take the responsibility of our retirement planning into our own hands.

The problem is, we tend to postpone our retirement planning thinking it is years away and that there would be time for that later. It could take years to save and plan for a comfortable retirement, depending on one’s income. There is no certain time point at which you have to “start” planning for your retirement, but the earlier the better. In fact, there is no harm in retirement planning from the very time you start earning.

2. The “When” question:

When is the right time to retire, really?

It may vary case to case, depending on many factors including: how early one started their career, loan status (if any), when one started investing, one’s lifestyle, family and dependents; and of course their jobs and incomes.

At the end of the day, there is no hard and fast rule on when to retire. It is the individual’s choice. This is a choice that has to be taken wisely, for one’s own good; and it is not to be influenced by societal pressures and opinions.

Retiring early is an unpopular opinion amongst many. Especially amongst those who are fortunate to have found their calling, and love their jobs or profession. Moreover, the global average life expectancy has increased to over 70 years in the past few decades, which has resulted in more people postponing their retirement.

On the contrary, there are also some people who eagerly anticipate and plan for an early retirement. For those who are self-employed, or have their own businesses to run (with the need of their constant presence), there is less chance of having a choice on when to retire.

This goes to show that there is no retirement age that is “too early”, or “too late”; to each their own.

3. The “What” question:

What is the best retirement plan?

The best retirement plan is to have multiple retirement plans.

By that I mean don’t put all your eggs in one basket. Retirement is essentially defined as leaving one’s job and ceasing to work. But that does not mean one’s income must completely cease too. Life is unpredictable and there are uncertainties looming around the corner at every stage of life.

Same with retirement. Everyone looks forward to the golden years of retirement where they can relax, do what they wish to and be stress-free. But with the worry that your retirement funds are not sufficient, that is not possible. That is why it is better to plan for multiple sources of passive incomes during retirement rather than depending on one.

Investing for retirement

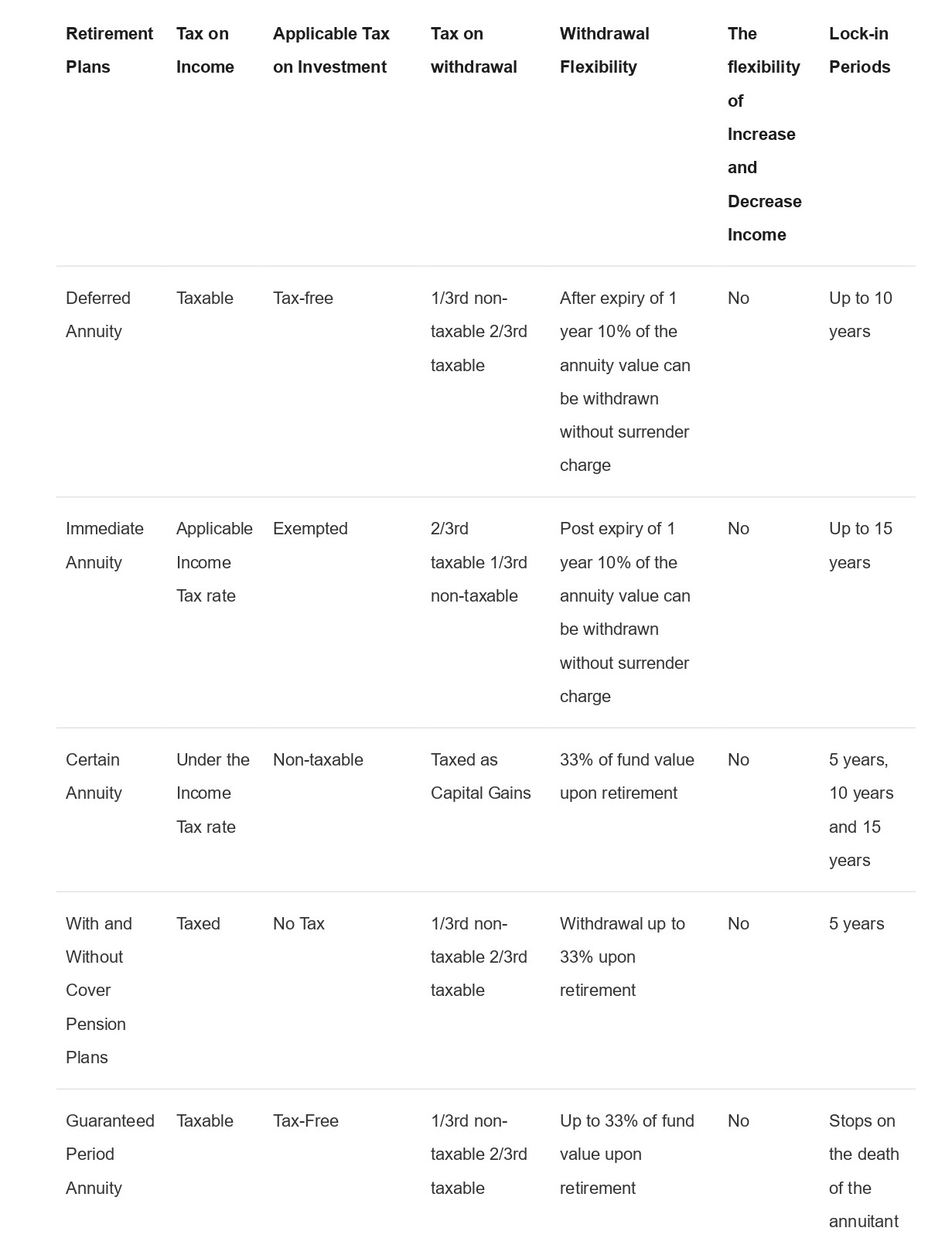

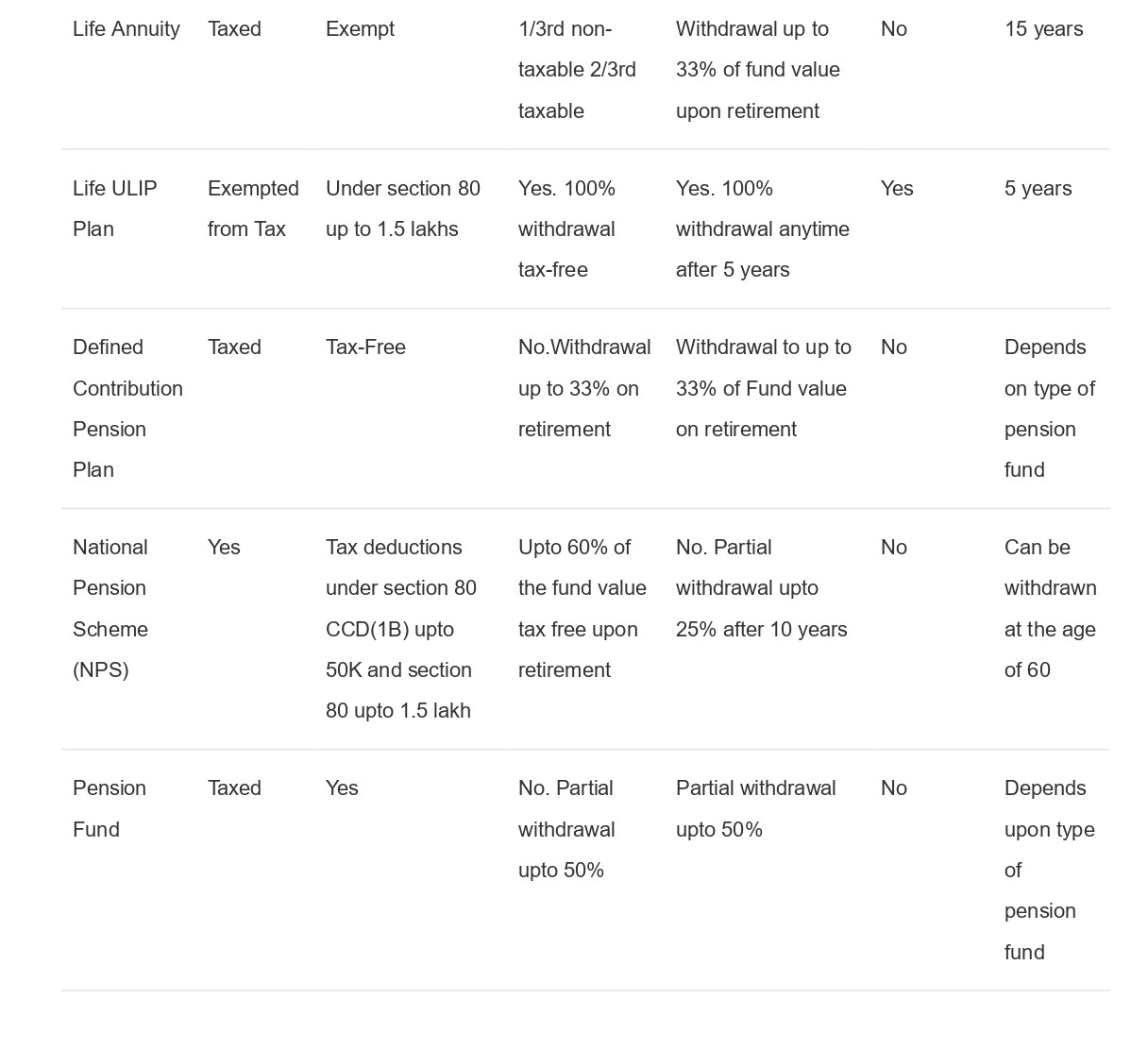

This again, is another reason to begin retirement planning early on. It is better to invest in a pension fund or pension plan early on to reap the maximum of its benefits. Here are some of the best pension plans available in India . There are various types and classes of pensions plans out there with its own advantages and disadvantages . Here is a comparison between the different pension plans that will give you an idea of the right choice for you-

Apart from pension plans, there are also investment strategies that could provide as an income during retirement. A sustainable passive income is a go-to in this regard. Passive incomes does not mean “getting something for nothing”. Of course you would have to initially put in the work to set it up, and also put in minimal efforts continually for it to work substantially. Here are 9 passive income ideas to help build your wealth and in turn increase your retirement income.

Saving your income

And last but not the least, SAVE YOUR INCOME!!

Many people make the mistake of splurging on unnecessary things come pay day. If all you want is an extravagant lifestyle, you can forget about retiring all together. Yes, it will be tough to cut-back on unnecessary expenditure at first. Surprisingly, spending frugally comes easily once you have plans for your future. I know that this lifestyle is not for everyone, but saving a portion of your income can go a long way in achieving your retirement goals.

4. The “How” question:

How do I start planning my retirement?

The first step is always the toughest to take. It can be confusing, and you might feel a little clueless (you would not be reading this article if you had a clear idea). Even though retirement is not just about financial planning, knowing how much money you will need to retire is the right place to start.

Sit down (by yourself or with a trusted friend/associate) and calculate a rough amount you would need as retirement savings, taking into account all possible factors. Use a retirement planning calculators to aid you with this.

The technical term for this is retirement corpus, which is the fund you need to have saved by the end of your work life to receive an adequate pension for your retired life. But by no means be alarmed or stressed by the number you will have to save! This is just a number to give you a personalized goal to reach. Knowing how much you need to save or invest now, is to help you make a plan to reach it so you can retire with confidence and security later.

Discuss with family

The second step would be to talk to your spouse, partner ,family, or even a close friend, as they would not only be part of your retirement but they can also help you think through this new phase from all perspectives. Again, it is not just enough to have a financial goal in mind. You also need to have a vision of what the rest of your life will look like. So it is important to discuss and ask important questions such as:

- Where will you live? Will you be downsizing and relocating?

- How do you want to spend your time? Will you work part-time?

- Discuss your dreams

- How much will you travel and where to?

- How will you serve your community?

- What’s your plan for visiting family and friends?

These discussions will help with having a clearer vision for the future and will help you navigate the upcoming changes and set specific expectations for yourself and the people you care about.

Get rid of Debt

The third step is a clear statement: Be Debt-free. Debt always means risk, and there is no room for risk in retirement. Take whatever measures needed to clear your debts (this includes mortgage).

Take a second job for a while, avoid unnecessary expenditure, sell your house and get a smaller place if you have to (to wipe out the mortgage or home loan), or even retire a little later than you planned.

Have Insurance and Emergency plans

The fourth, and probably the most important step, have a healthcare plan. This could easily be your first 3 steps if you get this early in life.

If you start investing early in your health insurance and term plans it works out a lot cheaper. And not just health in terms of insurance, start early on maintaining actual health. Maintain a healthy diet and lifestyle and continue with it so your health does not deteriorate quickly with age. But let’s face it: it is not easy getting old. Health issues and medical expenses are unavoidable.

Plan your Retirement Budget

The next step would be to make your retirement budget. This can be done as you are nearing your retirement. Based on your lifestyle, you will have to estimate how much you will be spending each month.

Be as specific as possible. Factor in everything including the things you talked about in step 2. As you near your retirement, you could also do a test run of your retirement budget for a few months.

In addition to your retirement budget, build up some cushion into your bank account by saving up an emergency fund. This will help cover untimely expenses, albeit one-time.

Another optional step would be to go to an investment professional or retirement planning expert. If you are not sure of your whens, wheres and whats of retiring, that is the way to go. Plus, it would be like having a good coach, who could help you plan and motivate you into putting it to action. There may be some game-time decisions that have a lot riding on them, and it is better to not do it alone!